US EV Fast Charging — Q1 2026

Paren’s Q1 2026 U.S. EV fast charging report examines infrastructure expansion, stable utilization, rising reliability, and the shift toward high-capacity, high-power networks as the market scales efficiently nationwide

Introduction

After a phenomenal 2025 by all measures, we enter 2026 with renewed questions about the pace of EV adoption and its overall impact on infrastructure investment and utilization. Will utilization continue to rise? Can the industry keep up with or exceed the 2025 pace of infrastructure buildout?

This report examines these questions and more with our continued focus on infrastructure, utilization, reliability, and pricing. Together, these metrics provide a clear view into whether charging networks are scaling sustainably and meeting real-world demand.

Paren was founded to address one of the industry’s core challenges: access to reliable, real-time intelligence on charging infrastructure performance. Today, Paren processes over 100 million data events per day and monitors more than 95% of U.S. DC fast-charging infrastructure in real time. This coverage enables a comprehensive, ground-level view of how charging networks operate across geographies, operators, and market conditions.

The following executive summary highlights the key findings from Paren’s Q1 2026 analysis with deeper detail shown in subsequent slides to back up these findings.

Finally, since we started this reporting journey in early 2025 we’ve heard from many of you in the industry that these reports have filled a gap in understanding the broad picture of the U.S. EV Charging market. We appreciate all feedback. Email us at hello@paren.app!

The Paren Team

Report Overview & Highlights—Q1 2026

Fast-charging networks enter 2026 with stable performance across key metrics

Q1 2026 reflects a market holding steady across infrastructure, demand, pricing, and reliability. Despite continued expansion, utilization remains within a tight range, pricing is stable, and reliability continues to improve—indicating controlled, sustainable scaling.

Infrastructure growth continues without disrupting utilization

Deployment remains elevated, with ~3,300 new ports added in Q1, in line with seasonal patterns. Utilization held at ~15.6%, only slightly below Q4, suggesting new capacity is being absorbed without overbuild—extending the supply-demand balance seen in 2025.

The industry is shifting toward higher-capacity, more efficient sites

Operators are prioritizing throughput over footprint, with fewer stations delivering more ports per site. High-power charging (250+ kW) dominates new installs, while site design is converging toward more standardized, economically efficient models.

National stability masks strong local variation

Top-line stability hides significant local differences. Utilization ranges from low single digits in underdeveloped regions to 25-30% in leading metros. Reliability varies more by operator execution than geography, reinforcing the importance of site-level fundamentals.

Pricing remains anchored as networks mature

Average prices held near ~$0.53/kWh in Q1 2026, with limited movement despite expansion and rising costs. Pricing remains tightly clustered nationally, with regional variation driven by structural factors. More advanced pricing models are expanding selectively in higher-utilization markets.

Review the following pages for in-depth analysis of these trends. For even deeper insights, please reach out to us at hello@paren.app for a demo, conversation, or general Q&A.

The Paren Team

Q1 2026 shows a fast-charging market scaling—while staying balanced

• Deployment remains elevated with 3.4K ports added in Q1

• Utilization holds steady at 15.6% despite expansion

• Demand continues to absorb new capacity

• Pricing remains stable at $0.53/kWh

• Reliability improves, with most markets in the 90–95% range

— The Paren Team

Charging Infrastructure Expansion

Charging Buildout Holds at Q1 Baseline—Post-Peak Reset Reflects Seasonality

Deployment normalizes in Q1 2026 after record Q4 2025 highs

Following a record Q4 2025, public fast charging deployments reset to 3,387 new ports in Q1 2026. While down from peak levels, activity remains consistent with Q1 2025—indicating seasonality and normalization, not a structural slowdown.

Fewer stations, more capacity—efficiency is improving

In Q1 2025, 721 stations delivered 3,331 ports; in Q1 2026, just 617 stations delivered 3,387 ports. This step-change indicates a clear shift toward higher-capacity sites, with operators energizing more ports per location rather than expanding footprint alone.

Buildout momentum continues into 2026

Q1 deployment levels show operators sustaining elevated buildout activity following 2025’s expansion. Growth is stabilizing quarter-to-quarter, but overall deployment remains well above prior-year baselines.

Site Capacity is Converging as Tesla’s Growth Slows & Others Scale Up

Convergence is driven by two-sided normalization

Tesla’s ports per station declined from its high of 15.0 in Q2 2025 to 12.2 in Q1 2026, reflecting a moderation after peak deployment intensity. In parallel, non-Tesla networks increased from 3.7 to 4.6, steadily scaling site capacity. This two-sided movement is compressing the gap, signaling convergence in how networks size new sites.

Tesla retains a structural advantage in high-density infrastructure

Despite this convergence, Tesla continues to operate ~2.7x higher ports per station, maintaining a clear lead in deploying large-format, high-throughput sites. This reflects a fundamentally different infrastructure strategy, prioritizing fewer, larger locations.

Industry is shifting from expansion to densification efficiency

The data indicates a transition away from pure network expansion toward optimizing capacity per site. Non-Tesla operators are increasing ports per station to improve utilization and economics, rather than scaling footprint alone.

Site design is approaching practical capacity benchmarks

After rapid increases through 2025, port density growth is stabilizing across both Tesla and non-Tesla networks. This suggests operators are converging toward repeatable, economically viable site configurations, with less variance in new deployments.

Note: For infrastructure counting, Tesla Supercharger For Business branded stations are included in the Non-Tesla numbers reflecting Tesla’s role as both a CPO and a hardware/software provider.

Growth is Broadening as Tesla’s Share of New Deployments Declines

Tesla remains the largest deployer—but no longer drives market growth

Tesla contributed 26% of new ports in Q1 2026, down significantly from peak levels above 40% in 2025. While still the single largest player, its influence on incremental supply is declining.

Growth is now distributed across a broader set of operators

Networks outside the top players collectively accounted for 30.4% of new deployments, making the long tail the largest contributor. This marks a shift from a concentrated to a fragmented growth model.

New entrants are scaling rapidly and reshaping the competitive landscape

Operators such as Ionna (8.2%) and Red E (7.8%) are contributing meaningful share, reflecting the rise of OEM-backed and retail-integrated deployment strategies. Six of the CPOs in the top 10 in Q1 2026 were not in the Q1 2025 top 10.

As the field broadens, execution—not scale—becomes the differentiator

With more players deploying similar infrastructure, competitive advantage is shifting toward site selection, reliability, and utilization performance.

New Infrastructure is Built for High Power

High-power charging now defines new deployments

250+ kW ports account for 55% of new installations, while sub-150 kW has declined to just 21%, marking a rapid phase-out of lower-power builds. Across all operators, 67% of new ports are now 250+ kW, confirming this is no longer a segment shift—but the industry standard.

Lower-power installations are rapidly phasing out

Operators are prioritizing higher-output equipment to improve throughput and reduce congestion, rather than continuing to deploy lower-power configurations.

Vehicle capability—not infrastructure—is becoming the constraint

As more sites support 250-350 kW+, real-world charging performance is increasingly limited by vehicle charging curves rather than charger capability.

Execution—not peak power—is the next differentiator

With high-power now standard, competitive advantage is shifting toward uptime, load management, and consistency of delivered charging performance—not just advertised speed.

NACS is Scaling—But Parity Requires a Structural Shift

NACS adoption is accelerating—but from a small base

NACS deployments reached 606 ports in Q1 2026, representing ~21% of new additions. However, NACS still accounts for just ~8% of the installed base (2,940 vs. 33,969 CCS ports).

Growth is additive—not yet converging

Non-Tesla operators continue to deploy CCS at ~3.5x the pace of NACS (2,102 vs. 606 in Q1 2026), meaning the installed base gap is still widening despite growing NACS adoption at the vehicle level.

Mixed infrastructure will define the near term

Operators are struggling to find the right mix of connector types for new and existing stations. Some are scaling back their plans and replacing NACS with CCS to improve station utilization. Others are prioritizing dual-standard deployments at the stall level. Meanwhile, adapters remain critical to ensure interoperability during this multi-year transition.

Utilization & Reliability

Utilization Sees a Seasonal Q1 Dip

Utilization remains resilient despite rapid capacity expansion in Q4 2025

Average utilization held within a narrow 15-16% range over the past year. Q1 2026 dipped to 15.6% from a Q4 peak of 16.5%, reflecting seasonality, the impact of continued infrastructure growth, and to a lesser extent, scheduled station maintenance and severe February weather.

Utilization follows a consistent seasonal pattern

Rates softened in Q2 as new capacity came online, rebounded in Q3 with summer travel, peaked in Q4, and eased again in Q1—indicating a stable demand cycle rather than structural volatility.

Flat averages mask a wide performance gap

The national average conceals significant variation across markets. High-utilization urban and corridor locations coexist with underutilized sites, resulting in a blended metric that does not reflect on-the-ground performance.

Utilization is Structurally Uneven—& Consistent Over Time

High-utilization markets remain consistent year-over-year

The same leading markets—District of Columbia, California, New Jersey, and Florida—top utilization in both Q1 2025 and Q1 2026, with similar levels, indicating persistent demand concentration rather than short-term variation.

The utilization gap remains wide and stable

Utilization continues to range from ~2-3% in low-density regions to over 35% in leading urban markets, a spread that has remained largely unchanged year-over-year.

A middle tier is emerging—but not closing the gap

More states now fall within an 8-14% utilization range compared to Q1 2025, reflecting growing baseline demand as infrastructure expands—but without reducing the gap between top and bottom markets.

Performance is structurally local—not national

The persistence of geographic patterns confirms that utilization is driven by EV adoption, urban density, and corridor traffic, making site selection the primary driver of network performance.

U.S. Fast-Charging Market Splits into Four Archetypes

Four market archetypes are emerging

The U.S. fast-charging market remains uneven. Leaders from Q1 2025—CA, WA, FL, and the Northeast—still dominate, while the interior stays underbuilt. A 2-3x performance gap persists.

- Healthy (CA, WA, NJ): High utilization with strong, improving reliability—the most mature model and national benchmark.

- Stressed (FL, NY, DC): Utilization above 25% with reliability starting to strain—where densification is most urgent.

- Pre-demand buildout (TX, CO, MN): Strong reliability but below-average utilization—infrastructure ahead of demand, with improving economics.

- Lagging (OK, rural markets): Low utilization and weaker reliability—driven more by execution gaps than demand.

Pricing adds a third lens

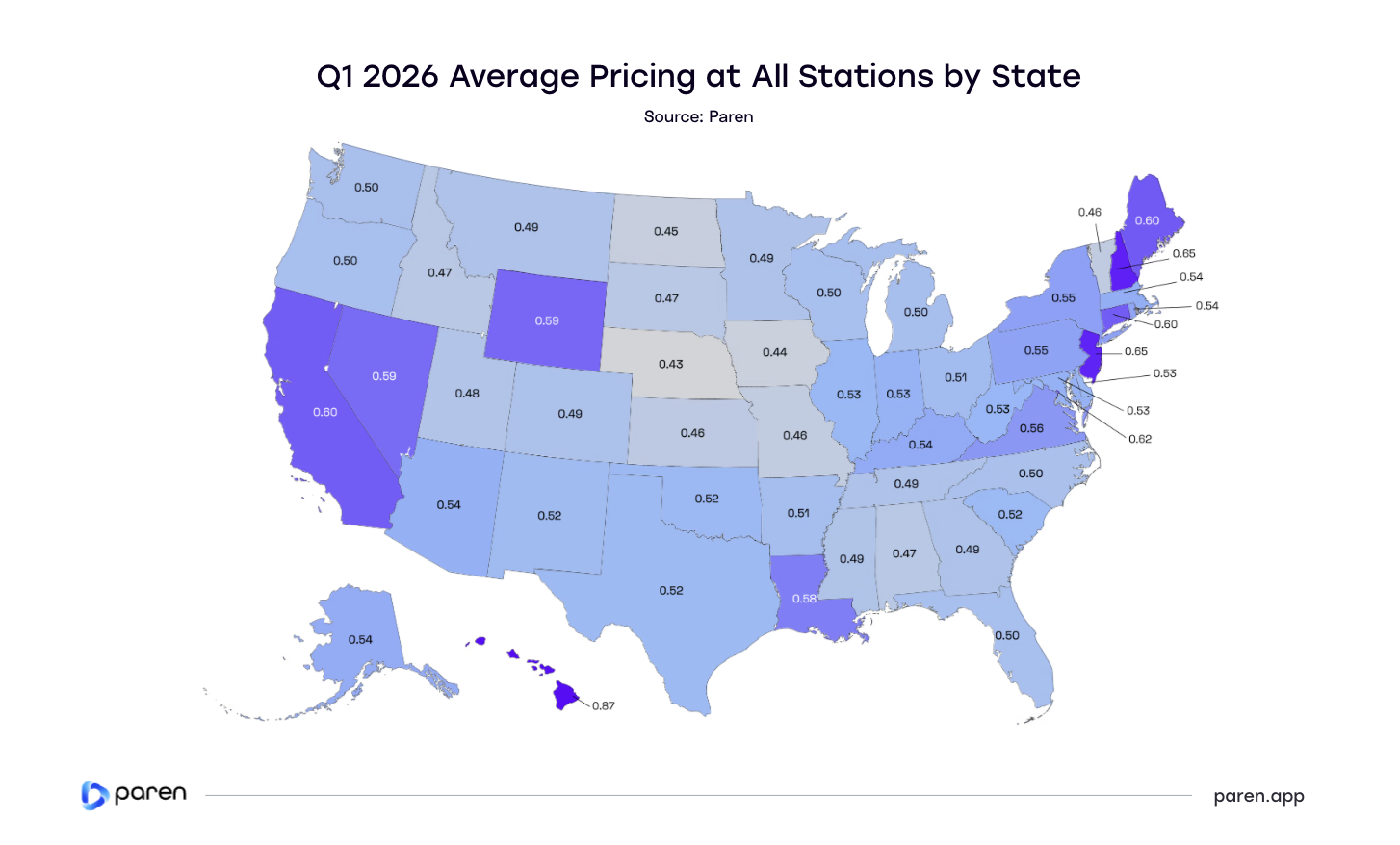

US pricing remains tight ($0.45-$0.60/kWh) vs. Canada’s wider range, with HI ($0.87) as an outlier. Lower prices still correlate with higher utilization.

Two dynamics to watch

Florida’s +14% price increase will test demand elasticity. Execution is emerging as the key differentiator, with new entrants reshaping the top deployers.

Infrastructure Keeps Pace with Demand—Despite Q1 Volatility

Continued session strength into 2026

Demand remained elevated into early 2026, with volumes rebounding to ~13.5M sessions in March after a February weather-induced dip.

Utilization operates within a defined equilibrium band

Sessions per Port (SPP) centers around a 200-220 monthly range—indicating balanced utilization without sustained congestion.

Q1 highlights seasonal demand swings

SPP fell to ~182 in February before rebounding to ~206 in March, consistent with winter softness followed by spring recovery.

Early signs of localized overcapacity—but not structural

The Q1 dip suggests capacity is temporarily outpacing demand in some markets, though March recovery points to continued underlying strength.

.png)

Reliability is Improving—but Not Yet Uniform

Reliability has improved across most markets year-over-year

Charging reliability has shifted upward, with most states now in the 90-95% range, compared to a broader 85-92% range in Q1 2025—reflecting gains from new builds, upgrades, and improved operations.

The performance floor is rising—but gaps persist

Lower-performing states improved from the 70-78% range in Q1 2025 to ~78-88% in Q1 2026, narrowing the gap but still trailing top-performing markets.

Underperformance remains concentrated in a few markets

States like Oklahoma (77.7% vs. 70.5% in Q1 2025) are slowly improving but continue to lag their neighbors, indicating persistent challenges in network quality and maintenance.

Variation is driven by execution—not geography

Unlike utilization, reliability leadership shifts across markets year-over-year, reinforcing that performance depends on operator execution, site quality, and maintenance practices.

EV Charging Pricing

EV Charging Prices Stay Stable—Even as Energy Costs Rise

Data note: See the “Methodology” section related to our updated pricing model.

Pricing remains tightly anchored year-over-year

Average fast-charging prices continue to fall within a narrow band of $0.45-$0.55/kWh, largely unchanged from Q1 2025. Despite network expansion and evolving pricing models, the market shows a highly stable national baseline.

Regional premiums are structural—not transient

High-cost markets—including Hawaii ($0.87), California (~$0.60), and the Northeast (~$0.60-$0.65)—remain consistently above the national average. These premiums align with higher energy costs and infrastructure constraints.

Florida loses incentives, prices rise

Florida saw a 14% price increase year over year primarily due to Florida Power & Light losing their incentive funding which was used to offset energy costs at their sites. These sites saw price hikes from 0.30 to 0.45 on January 1.

EV charging offers cost stability in a volatile energy environment

Unlike gasoline prices—which saw significant volatility in Q1 2026—EV charging prices remained remarkably stable at $0.53/kWh on average, reinforcing their role as a more predictable energy cost for drivers.

Pricing Remains Fixed—TOU Expands in High-Utilization Markets

Fixed pricing remains the industry baseline

Fixed per-kWh pricing continues to dominate, representing 77.1% of models in Q1 2026. It remains the default across most markets, especially in lower-demand regions where simplicity and predictability are prioritized.

TOU adoption is growing—but selectively

Time-of-use pricing accounts for 24.1% of pricing models, with adoption concentrated in higher-utilization states where demand variability and congestion make pricing optimization more valuable.

Adoption is highly market-dependent

High-demand states such as California, Virginia, Nevada, and Texas show significantly higher TOU penetration (often ~30-40%+), while lower-utilization markets (e.g., Montana, Wyoming, Oklahoma, Vermont, and Idaho) remain heavily skewed toward fixed pricing—highlighting a persistent structural divide.

Time-based pricing remains niche

Per-minute pricing represents just 2.7% of models, with usage largely tied to regulatory constraints or legacy deployments rather than active expansion.

Pricing sophistication follows utilization—not scale

The stability of these patterns suggests pricing innovation is driven by local demand intensity and congestion, rather than overall network size or growth.

Appendices

Appendix A

Charging Infrastructure

- CPO: Charge Point Operator.

- Fast Charging: Charging port of a minimum of 24 kW.

- NACS: North American Charging Standard; Tesla’s charging connector now adopted by many networks.

- NEVI: National Electric Vehicle Infrastructure program under the Bipartisan Infrastructure Law.

- MSA: Metropolitan Statistical Area.

- Connector: A charging plug conforming to CCS, CHAdeMO, or NACS (J3400) standard.

- Port: A charging unit with one or more connectors capable of charging oneEV.

- Station: A physical location with one or more EVSEs (charging ports).

Utilization & Reliability

- Reliability Index: The Paren-specific calculation that measures charger reliability taking into account recent successful charge sessions with and without retries, failed charge attempts, and station downtime over a specific time period.

- Tesla: Tesla is a reference to the Tesla Superchargers.

- Utilization: The percentage of tracked time spent on both successful and unsuccessful charging activity at a charger over the time period open per day.

EV Charging Pricing

- Fixed Price: Refers to a consistent rate per kWh for the entire charging day.

- Time of Use (TOU): Pricing changes based on the time of day with higher prices during expected peak demand time. It encourages off-peak charging and can help balance grid demand.

- Time: Charges by the minute or hour. Often used where energy-based pricing is restricted.

Methodology Notes

- New in 2026: In Q1 2026, we introduced a targeted set of refinements to improve the accuracy of several underlying calculations and better reflect real-world market conditions. These refinements are intended to provide a more accurate and consistent view of market trends. As a result, some figures may differ slightly from those published in earlier editions of this report.

- Infrastructure: We enhanced the methodology used to measure charging station growth and expansion versus the prior year. We also refined how new stations are identified, reducing reliance on AFDC open-date fields and incorporating additional signals that more accurately reflect when stations become active.

- Pricing: We updated our average pricing model to exclude free chargers from the calculation. While free charging remains an interesting part of the market, including it in average paid-pricing calculations created distortion from a small number of outlier locations. To preserve comparability, we also recalculated prior-quarter pricing figures using the updated methodology.

Data Sources

- AFDC

- Paren Public Charging Infrastructure Dataset

- Select NEVI RFP documents and award data

- Proprietary charging session / utilization models

Appendix B

Metropolitan Statistical Areas

- Atlanta: Atlanta-Sandy Springs-Alpharetta

- Austin: Austin-Round Rock-Georgetown

- Boston: Boston-Cambridge-Newton

- Charlotte: Charlotte-Concord-Gastonia

- Chicago: Chicago-Naperville-Elgin

- Cincinnati: Cincinnati

- Columbus: Columbus

- Dallas: Dallas-Fort Worth-Arlington

- Denver: Denver-Aurora-Lakewood

- Detroit: Detroit-Warren-Dearborn

- Houston: Houston-The Woodlands-Sugar Land

- Kansas City: Kansas City

- Las Vegas: Las Vegas-Henderson-Paradise

- Los Angeles: Los Angeles-Long Beach-Anaheim

- Miami: Miami-Fort Lauderdale-Pompano Beach

- Minneapolis: Minneapolis-St Paul-Bloomington

- New York: New York-Newark-Jersey City

- Orlando: Orlando-Kissimmee-Sanford

- Philadelphia: Philadelphia-Camden-Wilmington

- Phoenix: Phoenix-Mesa-Chandler

- Portland: Portland-Vancouver-Hillsboro

- Sacramento: Sacramento-Roseville-Folsom

- San Antonio: San Antonio-New Braunfels

- San Bernardino: San Bernardino-Riverside-Ontario

- San Diego: San Diego-Chula Vista-Carlsbad

- San Francisco Bay Area: San Francisco-Oakland-Berkeley

- Seattle: Seattle-Tacoma-Bellevue

- St Louis: St Louis

- Tampa: Tampa-St Petersburg-Clearwater

- Washington: Washington-Arlington-Alexandria

About Paren

Paren is a data intelligence platform for EV charging insights

As a neutral platform, Paren uniquely aggregates, enriches and standardizes fast charging across North America. We started these quarterly reports to provide EV charging leaders with a richer perspective on the broader industry dynamics using our unique data and insights.

We value your feedback, email us at: hello@paren.app

Paren provides granular insights on EV charging at scale

Paren is a real-time data platform for electric vehicle charging that standardizes reliability, availability, pricing, and amenities across networks. By covering over 95% of the US fast charging infrastructure, we process over 100M real-time events per day over more than 70K DCFC ports in the US and 7K DCFC ports in Canada. Our partners are automakers, charge point operators, map makers, ride share operators and government entities in need of rich and reliable data.

Offering historical data from January 2024 and real-time data

Our platform offers access to historical and real-time data using the following platforms:

- Flat files: Rich datasets for BI tools

- API: Real time access to granular insights

- Online portal: Self serve portal for specific projects

Interested in deeper insights?

- Follow Paren on LinkedIn ↗ link

- Check our blog posts ↗ link

- Read about Paren in the news ↗ link

- Track our monthly CPO/Network leaderboard ↗ link

Report Team

Want the data behind the data?

Access utilization, reliability, and pricing at the station level across 95%+ of US and Canadian DCFC infrastructure.