EVgo Q2 2025: Strong Results Despite Falling Utilization

.avif)

On Tuesday August 5, EVgo posted its Q2 2025 investor relations presentation, which included some very interesting charging industry numbers and metrics — that were also consistent with the data and analysis in our Paren Q2 2025 State of the Industry Report (SOTI).

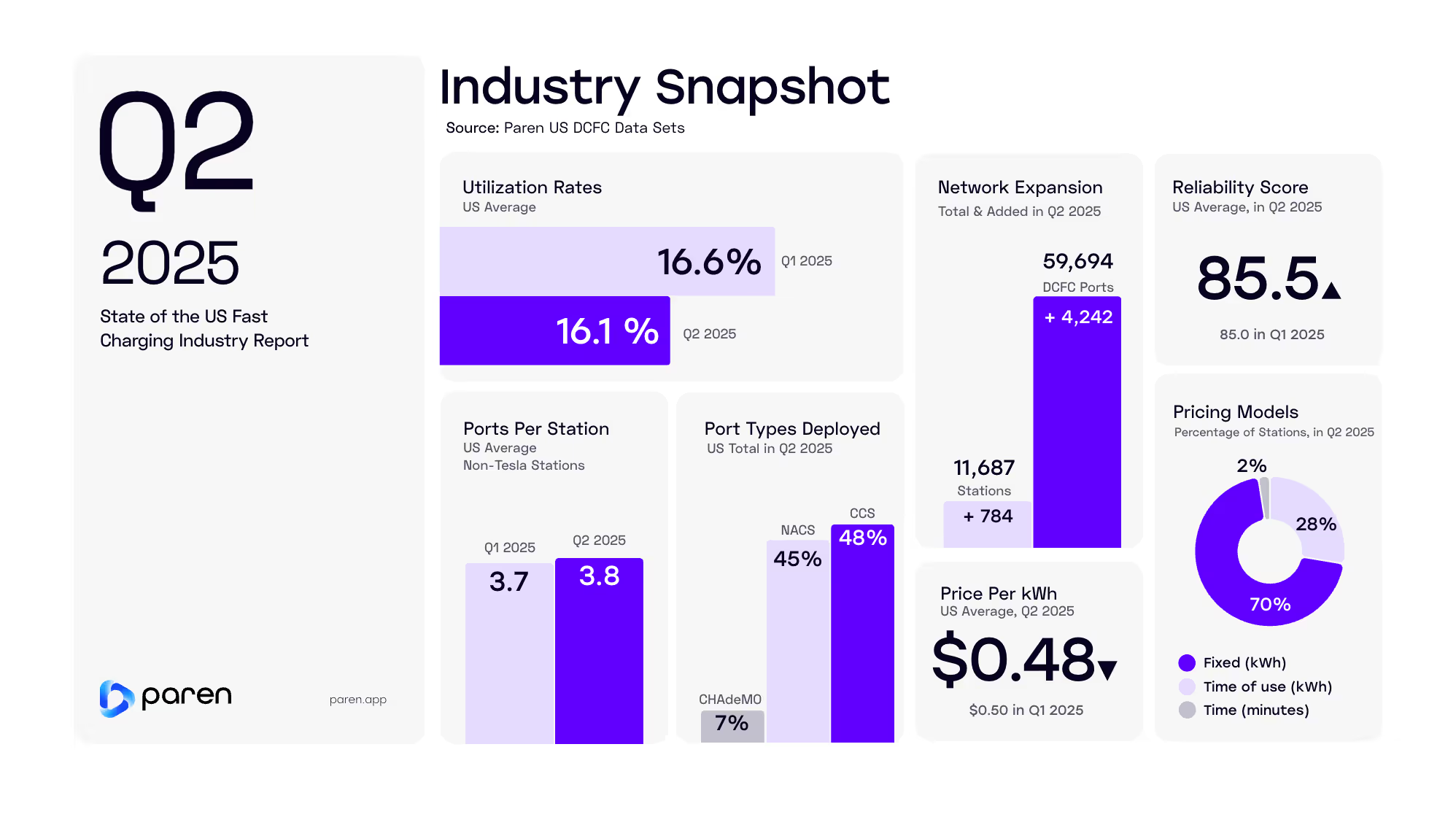

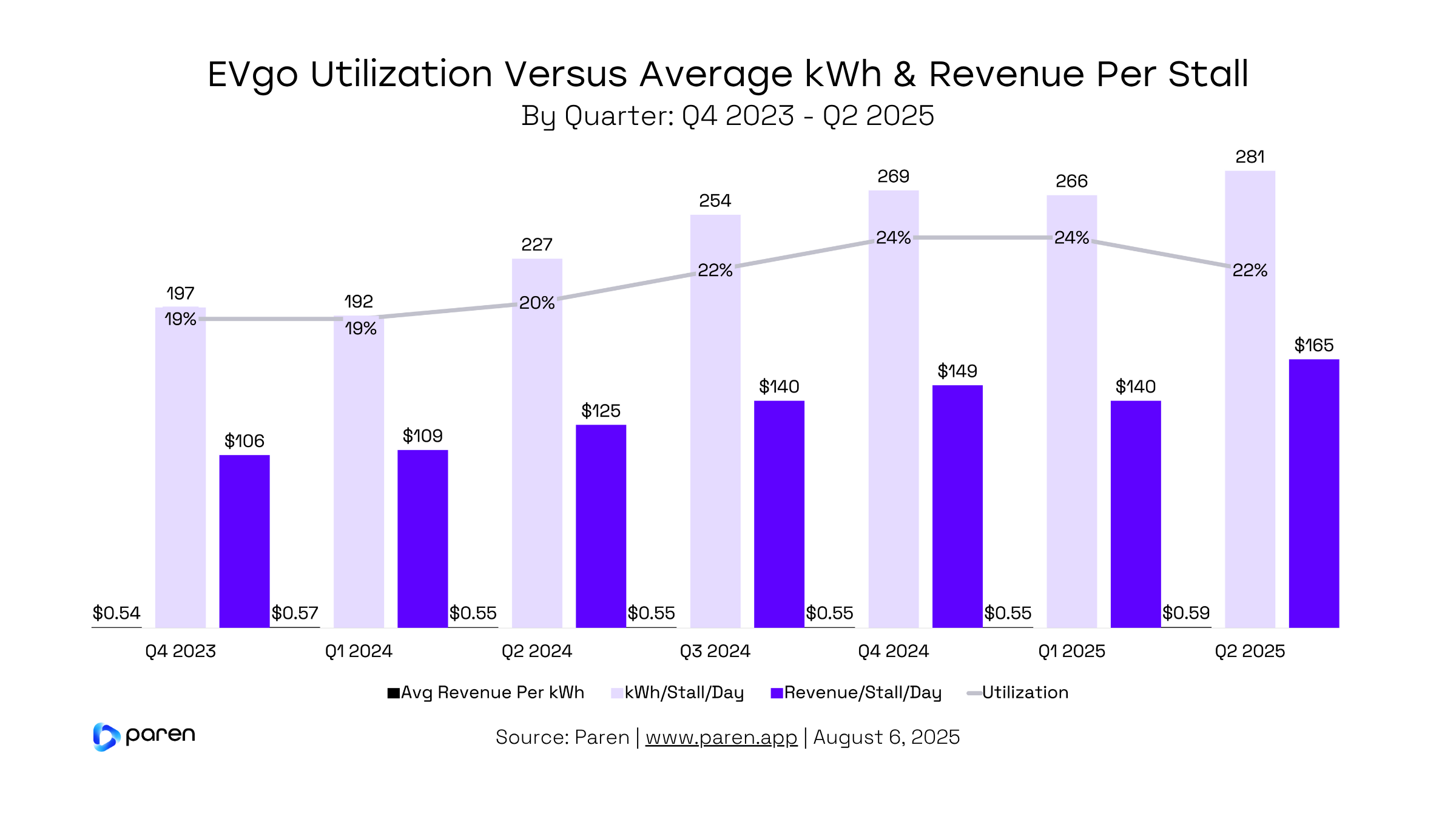

EVgo's utilization rate (measured as the number of charging minutes a day a stall is dispensing kWh/1,440 [minutes per day]) actually declined two percentage points to 22% in Q2 from 24% in Q1. In our Q2 SOTI report, we saw a US average decline to 16.1% from 16.6% in Q1.

However, despite a drop in utilization rate, EVgo saw its kWh Per Stall/Per Day (throughput) increase to 281 from 266 in Q1. Average Revenue Per Stall/Per Day rose to $165 versus $140 in Q1. And Average Revenue Per kWh increased to $0.59 from $0.55 in Q1.

EVgo's lower utilization combined with higher throughput, revenue and average price is largely a result of: higher pricing, seasonal effects (warmer weather = batteries charge faster = shorter sessions = lower time-based utilization), and the growing share of 350 kW chargers (now 57% of stalls) enabling faster charging sessions.

EVgo has funding to deploy 9,000 new stalls and appears well positioned to be among the winners in the industry. For many years the mantra was "build it and they will come." Now that average utilization rates are north of 20% for many CPOs, customer acquisition, experience, and retention along with price optimization and cost management become paramount.

We at Paren are excited about the changes happening and stand ready to help companies make smarter decisions, including session, utilization, reliability, pricing and amenities data. Reach out if you'd like to schedule a discovery call and demo.

By Loren McDonald, Chief Analyst - Paren